Hunting yield: Crypto Covered Options vs Lending

“I think investment psychology is by far the more important element, followed by risk control, with the least important consideration being the question of where you buy and sell.”

- Tom Basso, Trendstat Capital

With Bitcoin continuing to trade in what seems like an infinite range of choppiness, the hunt for yield and market neutral strategies continues.

This week we had a blast at Invest Asia in Singapore, where we could firmly see the market excitement over the theme in our last edition of Dark Pools – Lending.

In this edition of Dark Pools we want to uncover a more dynamic but early-stage topic.

I caught up with a good friend of mine, Bobby Ong, from Coin Gecko, who really put the idea in my head to write about this - thank’s Bobby.

Crypto Options as an Income Strategy

While it’s a vast and technical topic, I am going to make this as concise as possible. For the purpose of this edition we are going to specifically look at the use of ‘covered calls’ to generate consistent recurring income, and following that, we will analyse just how successful this strategy is in comparison to our last theme, Lending.

The Basics of Options

For those who are new to options, as Investopedia defines:

“An options contract offers the buyer the opportunity to buy or sell the underlying asset. Unlike futures, the holder is not required to buy or sell the asset if they choose not to.”

There are both call option (gives the holder the right but not the obligation to buy an asset) and put option (gives the holder the right but not the obligation to sell an asset), with numerous strategies to go about executing them.

Covered calls on BTC – a strategy for the ‘yield investor’

The covered call strategy is known as a neutral strategy. Similar to lending, it means that you aren’t expecting a substantial increase in price of the underlying asset.

The word ‘covered’ means that you already own the underlying asset that you are writing options against. If you don’t own the underlying asset, it is known as ‘naked’, which we may cover in a future edition.

Here is an example of how covered calls on crypto work.

The trade

You currently own 1 Bitcoin which is deposited in your Deribit account. The price is currently trading around $10,000 as of today.

In your belief, you think that Bitcoin likely will not rise to $12,000 by the 27th of September (this is the next expiry and only 15 days away).

With this in mind, you sell an ‘Out of the money’ call option with a strike of $12,000 and receive a credit of 0.019 BTC (roughly $195). This credit is now yours. You own it.

The expiry

There are two scenarios that can then occur when the 27th of September reaches.

Scenario 1: BTC ends above $12,000 strike price (exercised)

If, for example, BTC is at $13,000 on the 27th of September, your option that you sold can be exercised, meaning that you have to sell the BTC for the agreed price.

You still made a really healthy profit which equates to a total position of 1.019 BTC, and a USD value of at least $12,195. Effectively, your upside is capped at this figure. If BTC continues to go up, you won’t make any more money.

The person who bought the Call contract from you will effectively be able to buy that BTC off you for $12,000, even though it has a current market price of $13,000. They can close it out for a profit or let it ride.

Scenario 2: BTC ends below $12,000 strike price (not-exercised)

If on the 27th of September, BTC is at $11,000 for example, the option you sold will not be exercised and the person who bought it from you will be holding a worthless contract.

You get to keep the credit you received, keep your Bitcoin, and have just increased your asset-base by 0.019 BTC in 15 days. In addition to that, BTC is also trading at $1000 more than it was when you sold the call.

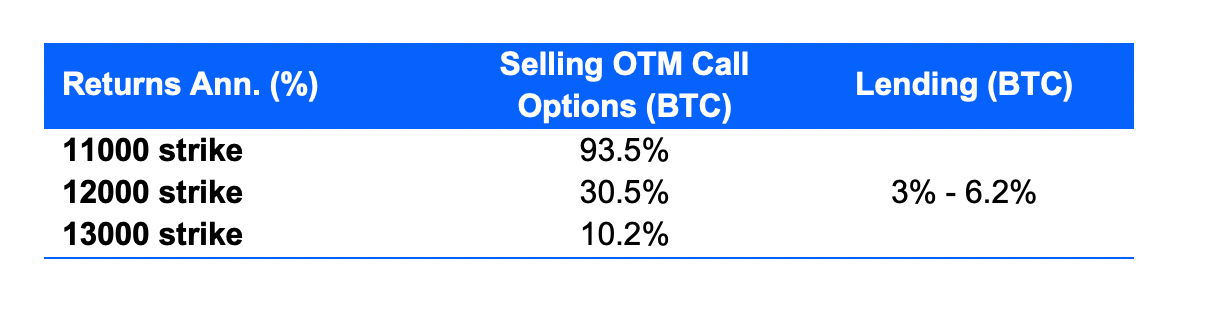

Options vs Lending - compare the yield.

Looking at BTC options on Deribit with respect to the above example, an out-of-the money (OTM) call option, expiring 27 sep (15d) @ 12000 strike, would cost 0.011 BTC.

This translates into a 1.1% yield for 15 days (30% ann.) for investors looking to sell those options.

If one were to lend BTC on Binance, the returns would be 0.001151 BTC (3% per annum.) per BTC across a 14d period. Hence for the option speculator, there is theoretically 10x more returns to be made if one was to sell OTM calls for a 30% annual rolling yield.

Based, on these metrics, the yield for writing BTC options is materially higher.

Note: It’s almost impossible to forecast consistent annual yields when writing options, hence we have extrapolated such returns by utilizing the same ‘rolling average premium of an OTM strike price’.

What about the risk?

Of course, the discussion above on options and outright lending is not an apple to apple comparison, and with several assumptions that has to be made. One might contemplate that the risk involved might be huge as options trading would not protect your initial principal as compared to lending. However, as fund managers, it’s all about the risk and reward, and we contemplate that the current yield disparity from selling options versus outright lending is too great to be ignored.

Another example if the former is not convincing enough..

Putting things in contrast, we refer back to the traditional markets. An Apple (AAPL) 15d OTM call option with a strike of 10% above its current price would cost 8 bps, while a similar option in BTC would be priced at a whopping 275 bps.

There are a-lot of moving parts.

We don’t want to fool you, options are complex and there are alot more to them than meets the eye. If you want to go down the rabbit-hole to learn about Strike Prices, The Greeks, Credit Spreads and more, check out a few of these links below.

About Covered Calls, Understanding the Greeks, Credit Spreads

Until next time,

Matt

Astronaut Capital

Talk to us about our new investment fund

Learn more about Astronaut Capitals’ new accredited investor liquid fund. The fund is open to institutions, family offices, corporate investment firms and select accredited investors.

About Astronaut Capital

Since 2017, Astronaut Capital has been one of the leading asset-managers for cryptocurrencies and digital assets. Utilizing its internal research team at Picolo Research and STO Rating, Astronaut operates long/short strategies to navigate the market on behalf of investors.

For subscription information about our investment funds, visit www.astronaut.capital or follow us on twitter.